NATIONAL INSURANCE SYSTEM

NATIONAL INSURANCE SYSTEM

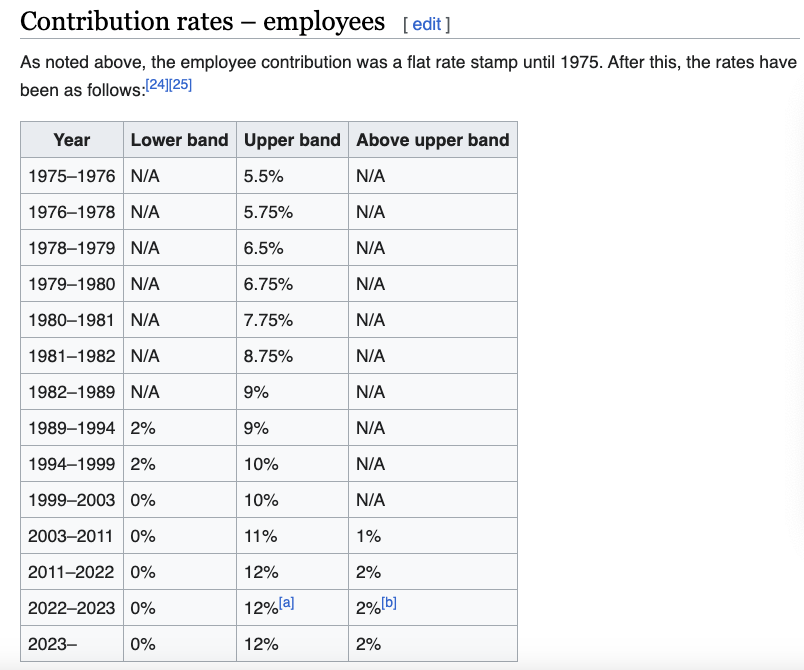

Better National Insurance Fund and contribution system

Better National Insurance Fund and contribution system

WOMEN FROM AGE 60 TO STOP PAYING

NATIONAL INSURANCE

WOMEN FROM AGE 60 TO STOP PAYING

NATIONAL INSURANCE

Remembering that although this means worker National Insurance contributions would end at age 60 for 1970s born women onwards, bosses still keeping paying employer National Insurance contributions no matter how old you work.

Men's pension age could be reduced to 65, so stop paying worker National Insurance contributions, but would need new law which takes years to reduce men's pension age from 65 to 60.

INCREASE WORKER NATIONAL INSURANCE ON TOP WAGED

- Increase worker National Insurance contributions on wages from £70,270 from current 2 per cent to 10 per cent, using name Upper Earnings (and adding name threshold).

Instead of the current frozen maximum salary threshold for worker National Insurance contribution rates of £50,270 that equates to current 40p higher rate income tax rate. - Have further threshold of worker National Insurance contribution rate, using name Maximum Salary threshold,

on wages from £200,270.

- Pay 12 per cent worker National Insurance contributions from maximum salary threshold threshold of £200,270 wages upwards

(now only paying 2 per cent).

OTHER SOURCE OF INCOME INTO NATIONAL INSURANCE PENSION SCHEME

- Bring back Treasury supplement at its pre-1981 level of

18 per cent of contributions. - Source: the late Tony Lynes.

LOWER WAGED WORKER NATIONAL INSURANCE on

WORKING CLASS WAGES & FOR BOSSES

WORKING CLASS WAGES & FOR BOSSES

- National Insurance credits from first £1 of wages up to our new (unfrozen) personal tax allowance of £16,960. Ending National Insurance Lower Earnings Level system.

- Starter worker National Insurance contributions of

1.85 per cent from £16,960 to £40,270. - Reduce for most workers National Insurance contributions to

5.50 per cent of wages between £40,270 to £70,270 a year.

Only those on wages above £50,270 now would see a rise from 2 per cent to 5.50 per cent. - Lower all charities' employer National Insurance contributions from

current 15 per cent (April 2025 - 2028 rate) down to 10 per cent. - Keep threshold at which businesses start paying National Insurance on a workers’ earnings lowered from £9,100 to £5,000 (April 2025).

- Employer National Insurance contributions at old rate of 13.8 per cent for both:

- Micro-entities of very small companies,

- with a turnover of £632,000 or less

- £316,000 or less on its balance sheet

- 10 employees or less.

- Small companies

- with a turnover of £10.2 million or less

- or with £5.1 million or less on its balance sheet and

- having 50 employees or less

* Basic income tax allowance would increase

£500 per year from next tax year, with our new government.Up til and including age 49, after which higher age related tax allowance of £3,000 on top of personal income and National Insurance tax allowances from age 50.

SELF EMPLOYED AND NATIONAL INSURANCE

- Class 4 National Insurance credits for profits below £16,960.

- Class 4 National Insurance contributions of 1.85 per cent on profits between £16,960 and £40,270.

- Class 4 National Insurance contributions of 5.50 per cent on profits between £40,270 and £70,270.

- Class 4 National Insurance contributions of 10 per cent on profits over £70,270.

- Class 4 National Insurance contributions of 12 per cent on profits over £200,270.

Class 4 NIC Rates were in April 2024:

- 6% on profits between £12,570 and £50,270

- 2% on profits over £50,270.

- It is up to our party's tax accountant consultants, to simplify tax system so are real world tax bills each year for self-employed.

NATIONAL INSURANCE AND

WORKING AGE BENEFITS

WORKING AGE BENEFITS

(UK resident Citizen and

non-citizen with permanent right to live and work in UK)

non-citizen with permanent right to live and work in UK)

- End National Insurance (NI) Lower Earnings Level.

- Replace with automatic National Insurance credits granted from first £1 of income, in or out of work or 'economically inactive' (neither in work nor on benefit), up to wage level of starting threshold for

National Insurance contribution worker payment.

- Entitles you to state pension and

working age benefits. - Gives right to Statutory Sick Pay to lowest waged, majority of which are women.

NATIONAL INSURANCE FUND

WILL ONLY BE FOR STATE PENSION

WILL ONLY BE FOR STATE PENSION

- All the other things than for the state pension that

National Insurance Fund contributions have been for,

to move into general taxation for funding (as the rich earning over £80,270 a year will pay more income tax). - Worker and employer National Insurance contributions to be only for state pension

(renamed National Insurance Pension). - Redundancy for workers of private firms that go bankrupt, to come from assets of the company, as first priority before all others the company owes money to, and not from National Insurance Fund.

- Incapacity benefit,

- widows' benefits,

- maternity allowance,

- guardian's allowance,

and - Jobseeker's Allowance

- whether income tax or stealth, indirect taxes.

You are on BETTERED NATIONAL INSURANCE page

Example in 2024 shows the gross inequality of those with most money paying less National Insurance contributions:

- you earn £1,000 in a week you’ll pay:

- nothing on the first £242.

- 8% (£58) on your earnings between £242.01 and £967.

- 2% (£0.66) on the remaining earnings above £967.

- This means your National Insurance payment will be £58.66 for the week.